Financial Fundamentals: Retirement & Life Expectancy

Our Financial Fundamentals series is here to help you take control of your finances.

We’ve already explored pension consolidation, annual tax allowances and the benefits of managing your personal cash flow. This month we take a look at the importance of considering life expectancy when making your retirement plans.

It may not be the most appealing of topics, but a reluctance to consider our own life expectancy can lead to skewed retirement planning, and risks retirees depleting their funds.

The good news, of course, is that we often have a higher life expectancy than we assume.

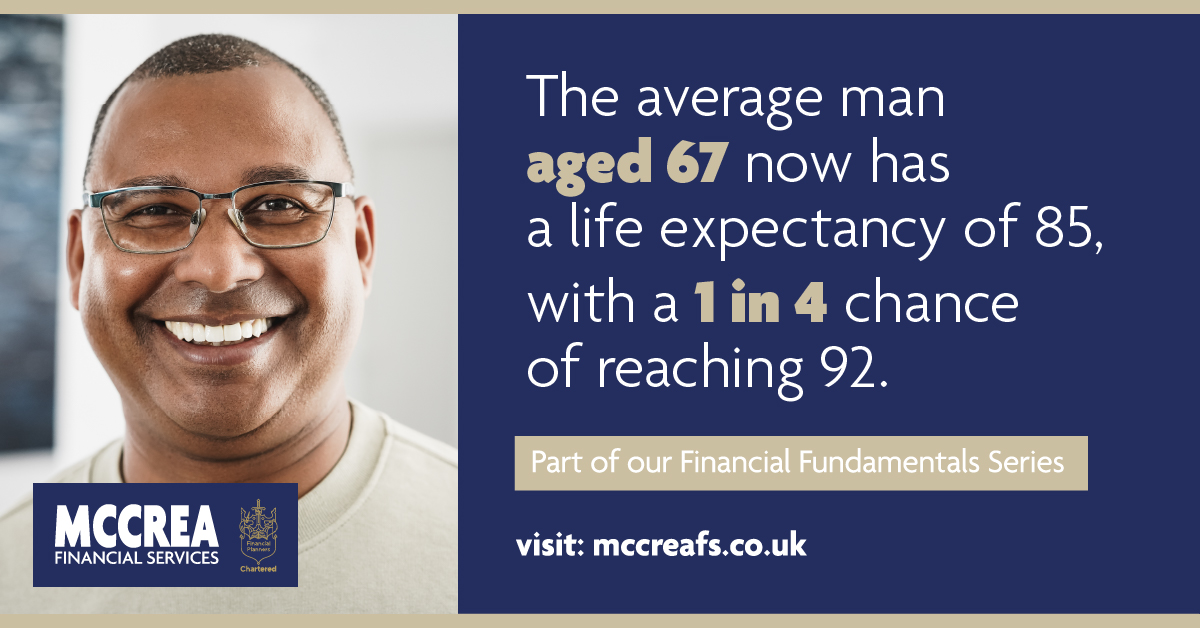

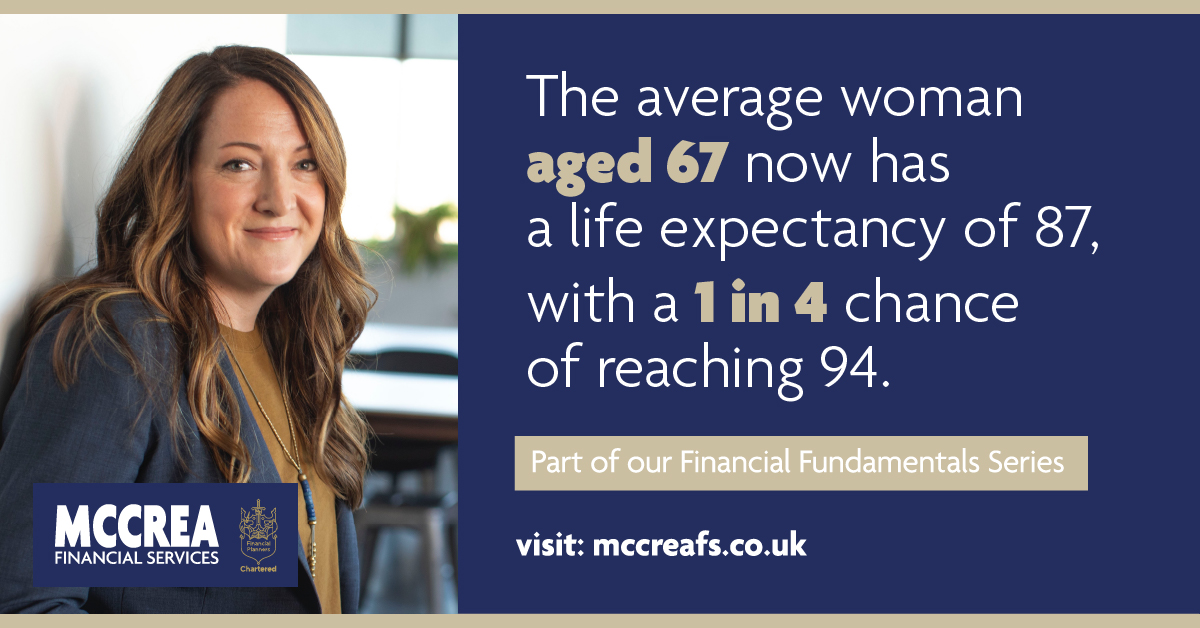

The Office for National Statistics (ONS) reports that a man currently aged 67 has an average life expectancy of 85, with a 1 in 4 chance of reaching the age of 92. The average woman currently aged 67 has an average life expectancy of 87, with a 1 in 4 chance of reaching 94.

Rising life expectancy means we can now expect to spend longer in our retirement than previous generations, with the average person now likely to receive their State Pension for 20 years.

Why is retirement planning important?

The downside of this change is that our perceptions of life expectancy still lag behind reality. As a result, we often fail to manage our income and assets in line with the most likely duration of our retirement. This can mean overspending in the early years of retirement, leaving little or no provision for later in life. Alternatively, lacking the confidence of a retirement plan which accounts for life expectancy can also lead to an over-cautious approach to spending which deprives you of the full enjoyment of your hard earned retirement.

How to create a retirement plan

While your entitlement to the State Pension will continue indefinitely once you reach the State Pension age, it’s essential to factor in life expectancy to your plans for private pensions, savings and other assets.

You can start by finding out your predicted life expectancy using the ONS calculator. While these predictions are not exact, based only on age and gender, they do take into account improvements in lifestyle, working practices and general health and wellbeing of the nation as a whole, and so can be a useful indication of how many years and decades you might spend relying on your retirement income.

Next, you can identify your required and desired retirement income based on the lifestyle you would like to enjoy. Keep in mind that your needs are likely to be different once you retire, when it’s likely you won’t have to make payments on a mortgage or commute to work.

Take advantage of expert retirement planning advice

Once you know the potential length of your retirement and the income you’d like to receive, you can create your tailored retirement plan. It’s widely advised that you consult a professional financial planner to help develop your retirement plan. Our expert team can work with you to identify your income targets, track down old pensions and make vital decisions on retirement age, pension consolidation and the balance between lump sums and monthly income.

Whether you have a retirement plan in place or haven’t yet started retirement planning, why not get in touch for a free no obligation consultation on how we can help you review or develop plans for the retirement you deserve?

You can also read our previous articles in the Financial Fundamentals series here: